5 minutes

5 minutes

Record high profitability on operational performance and positive refining environment;

Lower finance costs and FY17 dividend proposal of €0.40/share

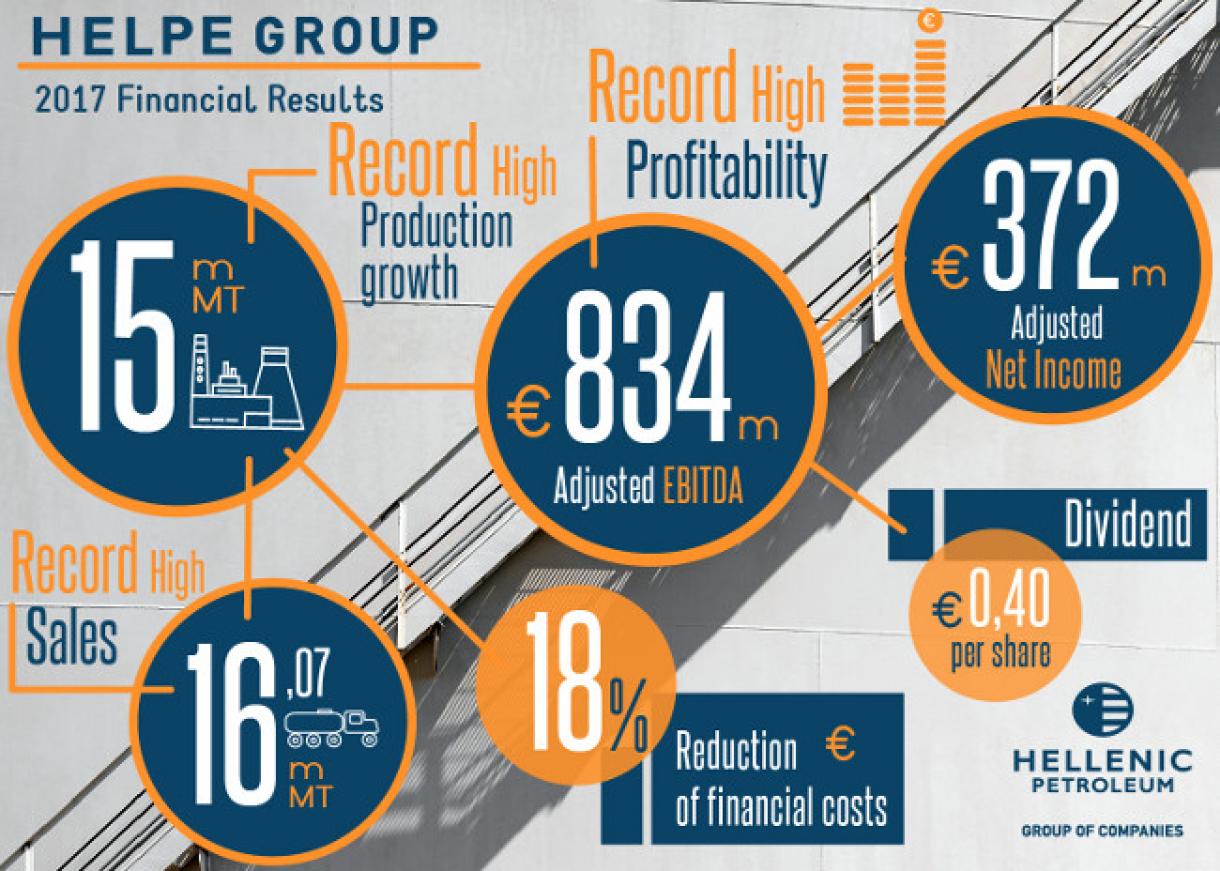

HELLENIC PETROLEUM Group announced its 4Q/FY17 results, according to IFRS. FY17 Adjusted EBITDA came in at €834m (+14%), the highest on record, with Group refineries improving utilisation and operations and achieving a record over-performance vs benchmark margins. Furthermore, the Group took advantage of the opportunities in the Med crude oil pricing structure, thus benefiting from significant savings in feedstock costs. Average benchmark refining margins remained at high levels, with the Group system margin increasing by $0.5/bbl, while the USD was slightly lower vs the euro.

The significant reduction of the Group’s financing costs by 18%, and the increased profitability of the affiliated companies, mainly due to DESFA’s performance, resulted to even larger improvement at the Adjusted Net Income level, which amounted to €372m (+40%).

Marketing and Petrochemicals divisions maintained their contribution at high levels, recording sales growth and improved performance. Adjusted EBITDA for Marketing was at €107m, with Petrochemicals at €95m for FY17.

In terms of FY17 Reported results, according to IFRS, the recovery of crude oil prices had a positive impact on inventory valuation, leading the IFRS Reported Net Income at €384m (+17%), as well as on Net Sales, which combined with sales volumes increase, amounted to €8bln (+20%), net of taxes.

With regards to 4Q17 results, the decline in benchmark margins and the appreciation of euro against the dollar, led Adjusted EBITDA to €170m (-21%) and Adjusted Net Income to €59m (-28%). Financing costs during the quarter recorded a further reduction for the 5th consecutive quarter, and at €37 million are down 28% vs 4Q16.

Considering financial results as well as 2018 outlook, the Board of Directors proposed to the General Meeting the distribution of a final dividend of €0.25 per share, which corresponds to a FY17 DPS of €0.40 (2016: FY €0.20 / share)

Higher crude oil prices and weaker benchmark margins in 4Q17

The recovery in crude oil prices continued in the fourth quarter, as OPEC announced the extension of the agreement for the control of crude oil production and exports. In 4Q17, Brent crude oil averaged $62/bbl, the highest level in the last two years, while in FY17 Brent was $10/bbl higher vs 2016, at $55/bbl.

The increase in crude oil prices, combined with the products supply, had a negative impact on Med benchmark refining margins, with FCC at $4.6/bbl (-15%), and Hydrocracking at $5.3/bbl (-3%). In FY17, margins were stronger with FCC averaging $5.9/bbl (+17%) and Hydrocracking $5.2/bbl (+ 4%).

Euro strengthened against US dollar in 4Q17, with the exchange EUR/USD rate averaging 1.18, while FY17 stood at 1.13.

Increased aviation and bunkering demand

In 2017 domestic fuels demand was 6.9MT, 1.9% lower compared to 2016. Aviation fuel consumption reached 1.15MT (+11%), growing for 5th consecutive year, while bunkering fuel demand increased by 18% to 2.8MT.

Improved operating cash flow, finance cost reduction, increased investments

In 2017, Net Finance costs amounted to €165m, the lowest levels in the last 5 years, following the refinancing of bonds and bank loans, and the reduction of Gross Debt by €600m over the last two years. Furthermore, the refinancing of loans maturing in 2018 is in progress, with a significant positive impact on the average cost and duration of debt, as well as improved risk management.

2017 operating cash flows (Adjusted EBITDA – CAPEX) amounted to €625m, recording a small increase vs FY16, despite higher capital expenditure (€209m), due to heavier refinery maintenance and competitiveness improvement projects. Net Debt came in at €1.8bln, at similar levels with the previous quarters.

Key strategic developments

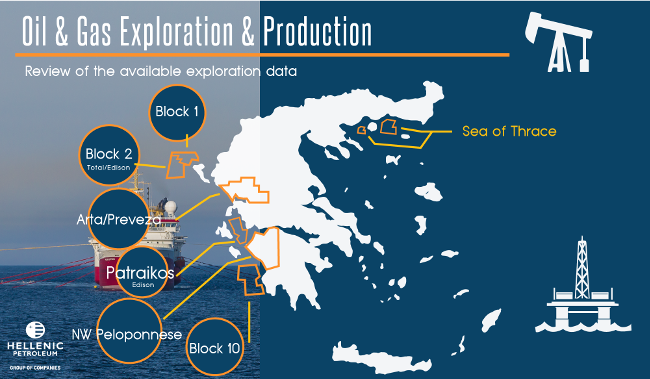

In Exploration and Production, the planned exploration works on the concession of the Patraikοs Gulf continues. Furthermore, the ratification of the Lease Agreements, for the onshore areas of Arta - Preveza and NW Peloponnese, as well as for offshore Block 2 by the Greek Parliament, is expected in the next few days, with the initial exploration works being scheduled to begin immediately after.

Regarding the participation in DESFA, the process for the sale of 66%, accounting for 35% of the Group's participation and 31% of the Greek State, is in progress. The two international JVs that qualified to participate in the final phase of the process, submitted binding offers on 16 February 2018, with ELPE and TAIPED currently evaluating the offers. In 2017, the participation of the DEPA Group in the consolidated financial results of Hellenic Petroleum amounted to €46m, with DESFA having a significant contribution.

Furthermore in 4Q17, the Group completed the acquisition of the 37% of the share capital of ELPET Balkaniki (owner of 80% and 81.5% of the share capital of the VARDAX pipeline and OKTA respectively), which it did not own, as well as 12 EKO Bulgaria stations, which were operating under long-term lease agreement.

Key highlights and contribution for each of the main business units in 4Q/FY17 were:

REFINING, SUPPLY & TRADING

- Refining, Supply & Trading 4Q17 Adjusted EBITDA at €130m (-23%), with FY17 at €639m (+19%)

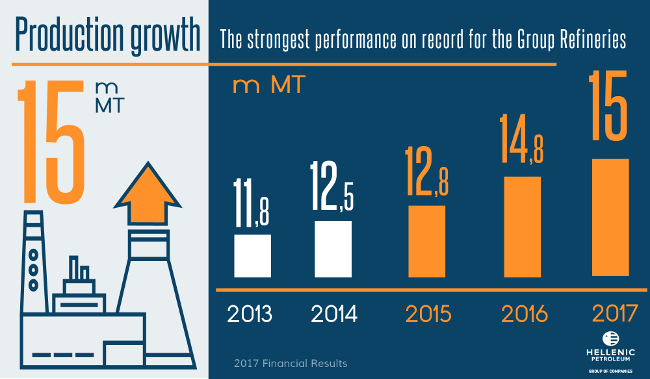

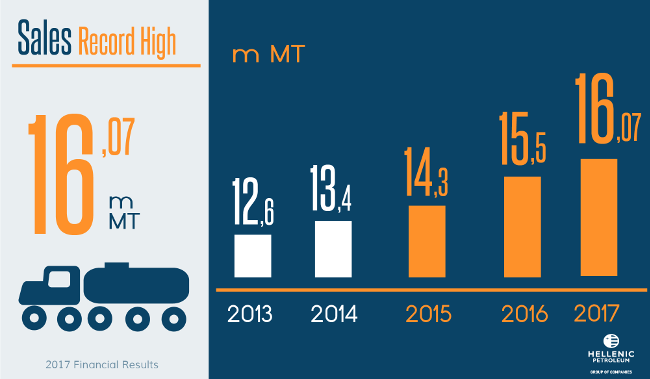

- The smooth operation of the refineries led to an increase in production and sales to 3.9m MT (+5%) and 4.1m MT (+7%) respectively in 4Q17,

- Total production and sales for 2017 came in at 15m MT (+1%) and 16.1m MT (+4%) respectively, with middle distillates yield at 48% and respective gasoline at 22%.

- Crude mix optimisation and improved operating performance led to a significant over-performance vs benchmark margins, offsetting the impact of the unplanned shut-down of the hydrogen unit at Elefsina refinery.

PETROCHEMICALS

- A small decline in polypropylene sales and stronger euro led to a decrease in the operating profitability, with 4Q17 Adjusted EBITDA at €20m (-20%).

MARKETING

- FY17 Marketing Adjusted EBITDA was €107m (+6%)

- Domestic Marketing volumes were higher by 3% to 1m MT for another quarter, with 4Q17 Adjusted EBITDA at €9m (-1%).

- International Marketing reported an increase in operating profitability, with 4Q17 Adjusted EBITDA at €13m (+10%).

ASSOCIATED COMPANIES

- DEPA Group participation to consolidated Net Income came in at -€1m, due to the increased provisions and lower sales volume.

- Elpedison EBITDA amounted to €14m (+19%), despite the delay in resuming the gas-fired generation flexibility remuneration mechanism.

Key consolidated financial indicators (prepared in accordance with IFRS) for 4Q/FY17 are shown below:

| € million | 4Q16 | 4Q17 | % Δ | FY16 | FY17 | % Δ |

| P&L figures | ||||||

| Refining Sales Volumes (‘000 ΜΤ) | 3,802 | 4,077 | 7% | 15,471 | 16,069 | 4% |

| Net Sales | 1,86 | 2,106 | 13% | 6,613 | 7,995 | 21% |

| EBITDA | 303 | 243 | -20% | 841 | 851 | 1% |

| Adjusted EBITDA 1 | 215 | 170 | -21% | 731 | 834 | 14% |

| Net Income | 145 | 111 | -24% | 329 | 384 | 17% |

| Adjusted Net Income 1 | 82 | 59 | -28% | 265 | 372 | 40% |

| Balance Sheet Items | ||||||

| Capital Employed | 3,903 | 4,173 | 7% | |||

| Net Debt | 1,759 | 1,8 | 2% | |||

| Leverage | 45% | 43% |

Note to Editors:

Founded in 1998, HELLENIC PETRELEUM is one of the leading energy groups in South East Europe, with activities spanning across the energy value chain and presence in 6 countries.

Further information:

V. Tsaitas, Investor Relations Officer

Tel.: +30-210-6302399

Email: http://[email protected]