5 minutes

5 minutesPositive results and improved outlook led to a

FY19 dividend proposal of €0.5/share

Accelerated strategy implementation

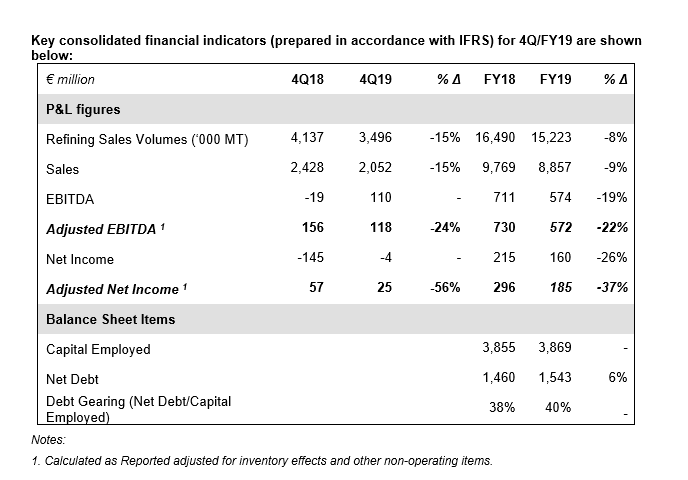

HELLENIC PETROLEUM Group announced its 4Q/FY19 financial results. 4Q19 Adjusted EBITDA came in at €118m, with FY19 at €572m, while FY19 Adjusted Net Income amounted to €185m. Results are satisfactory, considering increased international refining environment volatility and significant deterioration for most of 4Q19, as well as the planned 5-week turnaround at Elefsina refinery for its regular 3-year maintenance, which was safely and successfully completed in October. Improved operation, following start-up and better performance in other business units offset the negative impact of reduced production and sales during the turnaround period.

Furthermore, at the end of November, the Asporpyrgos refinery completed the transition to its new IMO operating model, supplying Greek bunkering hubs with low-sulphur, high quality marine fuels. During December, IMO FO sales amounted to 85k tons.

The BoD, considering the results, as well as the outlook for the Group, proposed to the AGM the distribution of a €0.25/share final dividend, resulting in a total FY19 proposed dividend of €0.5/share.

IFRS Reported Results were affected by the recovery of crude oil price in 4Q19, with an inventory gain of €4m vs losses in 4Q18, due to the material decline in crude oil prices in the respective period, with 4Q19 Reported EBITDA at €110m, vs €-19m in 4Q18. It should be noted that the results include as of 1 January 2019 the impact of new IFRS 16 on operating leases of retail fuel stations and other equipment.

Strategy implementation – Key developments

On 20 February 2020, the EGM of HELLENIC PETROLEUM approved a Memorandum of Understanding with the HRADF for the joint sale of the total share capital (65% HRADF – 35% ELPE) of DEPA Infrastructure, that will result from the partial spin off of gas distribution activities from DEPA Group, as well as the participation of HELLENIC PETROLEUM in the tender process for the sale of 65% of HRADF in DEPA Commercial, that will result from the restructuring of DEPA Group and will include the gas wholesale and retail activities. The agreement enables the Group to implement its strategy for divesting from gas distribution activities and minority participations, as well as grow in commercial gas activities.

In addition on 17 February 2020, the Group agreed the acquisition of a portfolio of PV projects with total installed capacity of 204MW in the Kozani area, Northern Greece from the German RES developer and contractor juwi. The project, upon completion of the construction process in 4Q21, will be the largest RES plant in Greece and among the 5 largest in Europe. The transaction accelerates the achievement of the target of 300MW of RES operating capacity earlier than scheduled.

Andreas Shiamishis, Group CEO, commented on results:

“2019 has been a transition year for the Group, with a number of business and organizational challenges. During the last months we proceeded with a series of initiatives that enable focus on our transformation strategy, such as the agreement with the HRADF for our participation in DEPA, the agreement for the acquisition and construction of the largest RES project in Greece, with an effective tariff, which is lower than system energy prices, as well as the planning for the strengthening of our international trading activities. Furthermore, we recorded progress on the governance and organizational fronts, through the amendments of our articles of association and the reorganization of our business activities and management team, introducing a simpler and functional structure.

Regarding results, the Group faced, for the first time after several years, a severe deterioration of the refining environment. In such a backdrop, we responded very successfully, improving our balance sheet and maintaining high returns for our shareholders. The issue of a 2% €500m Eurobond came at the lowest interest rate for the Group in more than 10 years and opened the international bond market for other Greek corporates. Furthermore, we updated our strategy, focusing on improving competitiveness, though operational excellence and new investments, as well as growth in new activities that will improve our environmental footprint by 50% until 2030, materializing our vision to play a key role in the energy transition in the East Med. I would like to thank all our employees for their efforts that made these achievements possible.”

Deterioration of refining environment

International crude oil prices recovered during 4Q19, reflecting mainly macro developments and supply/demand balances, with Brent prices averaging at $62/bbl, lower vs 4Q18 ($68/bbl). Equally on a FY basis, prices moved higher from the lows recorded in January 2019, with Brent at $64/bbl, vs $72/bbl in 2018.

The US dollar maintained its strength during the quarter, with EUR/USD exchange rate at 1.11, while in FY19, euro averaged at 1.12 vs 1.18 in 2018. A stronger USD benefits our international and export oriented business model.

The international refining environment deteriorated significantly during 4Q19. HSFO cracks declined to the lowest levels on record, with the launch to the market of the new compliant VLSFO, ahead of IMO implementation. White products cracks were lower vs 3Q19, with the exception of naphtha. Brent-Urals spread improved slightly, however remained at low levels on average. Those led to a significant deviation among refining benchmarks, with FCC margins averaging at $1.6/bbl, with Hydrocracking margins at $6.6/bbl, the highest in four years, highlighting the importance of the investment at Elefsina refinery, in view of global trends for cleaner fuels.

Increasing demand for domestic fuels market

Domestic fuel demand in FY19 was up 3% at 6.9m MT, the highest in the last 3 years, as both auto-fuels and heating gas oil consumption increased. Aviation and bunkering fuels grew significantly (+10%), at 4.6m MT, mainly driven by marine fuels.

Strong balance sheet, improved capital structure, reduction in finance costs

The new €500m Eurobond issue, combined with the partial refinancing of 2021 Eurobond through a tender offer, as well as improvements in bank loans commercial terms, strengthened our balance sheet and reduced financing costs by 21%, which is expected to continue in 2020. As a result, Net Debt stood at €1.5bn, at the lower end of the Group’s target range, with gearing ratio at 40%.

Key highlights and contribution for each of the main business units in 4Q/FY19 were:

REFINING, SUPPLY & TRADING

Refining, Supply & Trading 4Q19 Adjusted EBITDA at €76m (-39%).

- Net production amounted to 3.2m MT (-17%), with sales at 3.5m MT (-15%), with FY19 at 14.2 and 15.2 respectively.

- Realised ELPE system margin came in at $8.6/bbl in 4Q19, a significant over performance vs benchmarks.

PETROCHEMICALS

- 4Q19 Adjusted EBITDA came in at €20m (-9%), as operational performance and increased integration with Aspropyrgos refinery mitigated the impact of weak benchmark PP margins.

MARKETING

- In Domestic Marketing, improved performance in Retail and Aviation led 4Q19 Comparable EBITDA at €3m, with FY19 at €49m (+14%).

- International Marketing Comparable EBITDA at €15m (+44%), on account of improved in-market operations and supply optimisation, with FY19 at €56m (+11%).

ASSOCIATE COMPANIES

- DEPA Group contribution to consolidated Net Income was €21m for FY19.

- ELPEDISON EBITDA amounted to €20m in FY19, almost flat vs 2018.