5 minutes

5 minutesImproved results on higher production and exports, amid negative oil price environment and covid-19 crisis

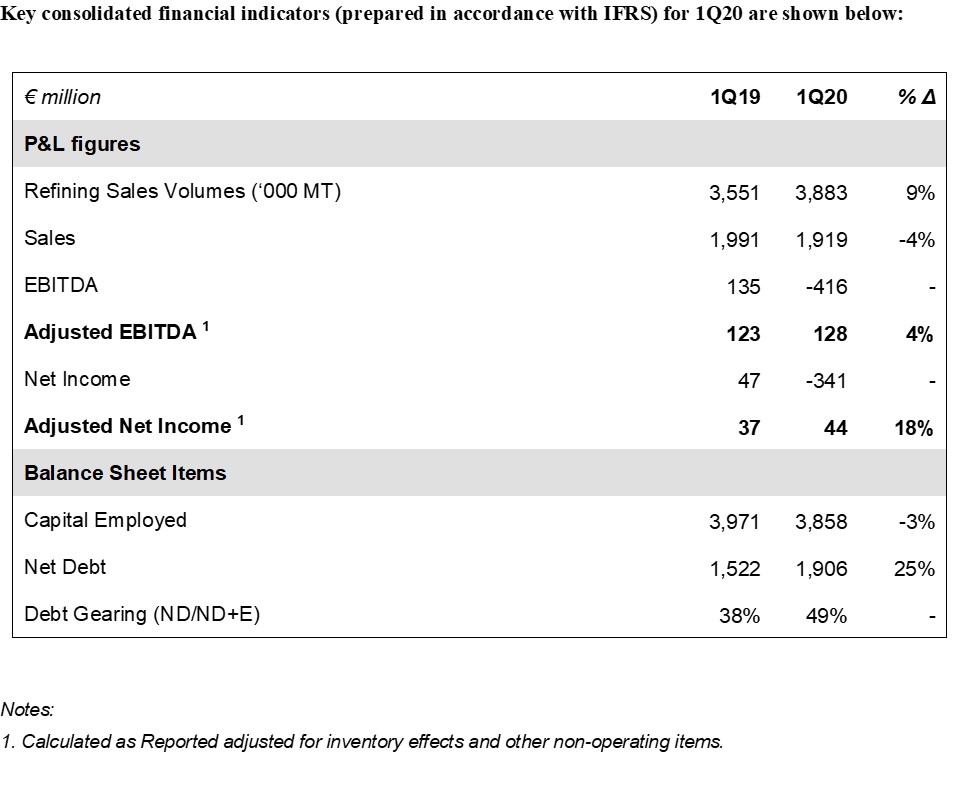

HELLENIC PETROLEUM Group announced its 1Q20 financial results, with Adjusted EBITDA 4% higher, at €128m and Adjusted Net Income amounting to €44m (+18%).

Refining environment was driven by increased volatility and the covid-19 pandemic, especially at quarter end; improved Refining and Fuels Marketing performance outweighed the negative impact of crude oil and feedstocks’ pricing, as well as the weaker domestic market sales due to covid-19. Increased refining availability led exports higher by 27% and total sales at 3.9m MT (+9%). Aspropyrgos refinery successfuly completed the first full quarter of IMO operation model, supplying the market with the full range of products, with a substantial change in the crude mix and required adjustments on operation and working capital.

The significant drop in crude and oil product prices by approximately 50% between December and March, to the lowest levels of the last few years, affected IFRS Reported Results, resulting in inventory losses of €540m, leading Reported Net Results to €-341m. It is noted that losses would have been higher, had the Group not proceeded with an inventory management program, already from 4Q19.

Covid-19 impact and response – Key developments

The outbreak of the pandemic and the measures implemented globally are having a significant impact on the economy, affecting the international energy sector. It is estimated that world demand decline, during restrictions on mobility and economic activity will reach or even exceed 20% in 2Q20, leading to a significant drop and volatility in crude oil and product prices; combined with the inability of existing storage capacity to absorb the supply surplus, resulted in an agreement from oil-producing countries for a c.10mbpd output reduction from May, while many refineries internationally are reducing runs or shutting down in 2Q20. The Greek market is also affected, with the decline in auto-fuels demand during April estimated at approximately 40%.

The Group proceeded with a series of measures to manage the crisis, already from end of February, with key priorities the health and safety of all staff and contractors, the smooth operation of facilities for uninterrupted market supply, ensuring sufficient liquidity and managing risks, as well as capturing opportunities in the contango pricing structure of crude and products. A policy for the prevention and response to the impact of the pandemic was established, with continuous information updating for employees, regular disinfection at facilities and offices and provision of personal protection equipment. Furthermore, refinery shifts were adjusted and a new teleworking model (WFH) was adopted for the vast majority of head-office staff, utilizing digital technologies.

The Group has a strong balance sheet, with sufficient liquidity at the start of the crisis. Since the beginning of March, in the context of risk management for the pandemic, the Group’s access to credit, from Greek and international banks, grew by €300m, which combined with the utilization of existing facilities headroom, resulted in a total liquidity increase since the beginning of the year of €550m, to help manage the crisis. Furthermore, finance expenses are at historic lows, recording a further significant reduction of 21%, to €26m in 1Q20.

In terms of its strategy, the Group is assessing the impact of the crisis and will adjust its business planning accordingly. Growing in the energy sector and improving carbon footprint by 50% in the next 10 years, remain key priorities, despite any delays due to the crisis. Design and implementation works for the 204MW Kozani project, as well as the sale process of DEPA subsidiaries (Commercial and Infrastructure) in which the Group is involved are in process. It is noted that during 2Q20, the corporate restructuring of DEPA SA, with the spin-off of international projects and the demerger of DEPA Infrastructure was completed.

Andreas Shiamishis, Group CEO, commented on results:

“In 1Q20 we managed to improve our operational performance and financial results in almost all our activities, while continuing the fast implementation of our strategy. Despite the notable recent developments in the oil industry, there is no doubt that the event that will define 2020 is the covid-19 pandemic and its impact on the world economy. Already from the first weeks of the crisis, we witnessed unprecedented changes in international supply and demand levels, with respective impact on prices. The crisis will continue to negatively affect most economic activity sectors, especially tourism that is more relevant to our markets.

The Group was among the first to take necessary measures, achieving uninterrupted operations, in the safest possible conditions for our personnel, which successfully responded to the challenge of transitioning to a different operating model. Furthermore, with full awareness of our responsibility to the Greek society, we designed and implement actions totaling €8m, aimed at supporting the national health system and vulnerable groups, that are most affected during this period.”

Deterioration of refining environment

International crude oil prices moved lower throughout 1Q20, recording a significant decline in March, as the impact from covid-19 and OPEC+ not agreeing to extend its production cuts escalated, with Brent prices averaging at $50/bbl in 1Q20, while in March Brent came in at $32/bbl, the lowest since 1Q16.

The US dollar strengthened further vs the euro, reflecting international macro developments; euro averaged at 1.10 in 1Q20.

White product cracks were lower vs 4Q19, due to weak demand, while HSFO cracks recovered strongly from the historic lows of 4Q19. Brent-Urals widened significantly to the highest levels in the last 9 years, with a positive impact on benchmark refining margins. As a result, FCC margins averaged at $3.8/bbl, with Hydrocracking margins at $5.2/bbl.

Weaker domestic fuel demand

Domestic fuel demand in 1Q20 was 4% lower at 1.7m MT, with auto-fuels consumption recording a respective decline, due to the negative impact of covid-19 on-demand in March. Heating gasoil, despite strong demand in March, due to mobility restrictions, was also lower in 1Q20, on mild weather in January-February. Aviation and bunkering fuels were 18% lower, to 681k MT. The negative trend of 1Q20 is expected to intensify in 2Q.

Strong balance sheet, liquidity management

The Group took advantage of favorable international capital markets conditions for the strengthening of its balance sheet, with the €500m Eurobond issue in 4Q19, achieving a material increase of its liquidity. Furthermore, at the initial signs of the crisis, proceeded to the additional improvement of its debt headroom, with new credit facilities of €200m and an increase of its LC issuance capacity for crude supply. Net Debt came in at €1.9bn, with gearing ratio at 49%, mainly due to the commodity price drop and the working capital increase.

Key highlights and contribution for each of the main business units in 1Q20 were:

REFINING, SUPPLY & TRADING

Refining, Supply & Trading 1Q20 Adjusted EBITDA at €86m (+8%).

- Net production 8% higher to 3.9m MT, with a respective increase in sales which came in at 3.9m MT (+9%).

- High-value product output increased, as IMO FO production was higher at Aspropyrgos refinery, minimizing HSFO production respectively.

PETROCHEMICALS

- 1Q20 Adjusted EBITDA came in at €20m (-22%), on account of weaker benchmark PP margins.

MARKETING

- In Domestic Marketing, improved Retail performance resulted in higher Adjusted EBITDA of €12m, mitigating the impact of weaker demand at the end of the quarter.

- Higher sales and improved operational performance in International Marketing led Adjusted EBITDA to €15m (+29%).

ASSOCIATE COMPANIES

- DEPA Group contribution to 1Q20 consolidated Net Income (excluding the positive impact of BOTAS case arbitration) came in at €15m.

- ELPEDISON 1Q20 EBITDA was 58% higher, at €17m, due to higher production and supply optimisation.