5 minutes

5 minutesOperating profitability significantly higher vs 1H19, with consistent improvement in financials; Interim dividend of €0.25/share

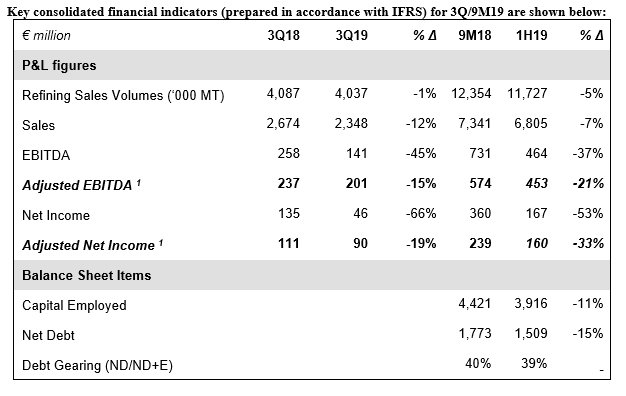

HELLENIC PETROLEUM Group announced its 3Q/9M19 financial results in accordance with IFRS. 3Q19 Adjusted EBITDA came in at €201m, a notable improvement vs last quarters, while Adjusted Net Income amounted to €90m. Higher total production, at 4.3m MT and good operations at refining units, despite end of run performance ahead of scheduled shut-downs and IMO test runs, resulted to sales exceeding 4m MT. Equally, improved performance in Domestic and International Fuels Marketing had a positive contribution.

The BoD, considering the strong results, as well as positive outlook for the Group, decided the distribution of an interim dividend of €0.25/share, payable in January 2020.

Performance was also positively affected by improved refining environment, despite weaker benchmark refining margins compared to historical highs recorded in recent years, as well as the restoration of the Russian crude oil supply infrastructure in Central Europe and a strong US dollar vs the Euro.

IFRS Reported Results were affected by crude price movements, which in 3Q19 dropped to the lower levels of the last two years, leading to a 12% drop in Revenues to €2.3bn. Equally, impact on Net Income was also negative, with inventory valuation losses of €43m, vs €53m gains recorded in 3Q18, as prices then increased. It should be noted that the results include for the first time the impact of new IFRS 16 on operating leases of retail fuel stations and other equipment.

The Group continued to improve its financial position, with finance cost further dropping by 25% y-o-y in 3Q19, at €27m, mainly on account of repayment of the €325m Eurobond issued in 2014. Furthermore, during the quarter, the Group proceeded to the successful issue of a new €500m, 2% Eurobond, with partial refinancing of existing bonds maturing in 2021. The transaction is expected to lead to an additional annual decrease in finance costs of approximately €15m, with total reduction exceeding 50% in the last 3 years, with a notable impact on the Group’s cash flow profile and dividend distribution capacity.

Andreas Shiamishis, Group CEO, commented on results:

“Improved 3Q19 results, the strongest of last 3 quarters, are particularly encouraging, on the back of a material improvement in environment. We are operating in a highly cyclical industry, without the ability to influence international developments. As a result, it is important to focus on issues we can control through strategic direction, managing and operating our business units and improving competitiveness. Despite 2019 being the most challenging refining environment in the last few years, our results and financial position are strong. On a positive note, domestic fuels market recorded a 3% growth. We consider the short term outlook to be positive, with the introduction of new bunkering fuel specs; our recent performance in capital markets, with the successful Eurobond issue in 3Q19, further confirms the confidence of the domestic and international investor community in HELLENIC PETROLEUM. I would like to thank once again the management and employees for their significant contribution to our successful performance.”

Volatile refining environment and stronger USD

Global macroeconomic developments, especially around international trade relations, led to weaker crude oil prices, with Brent averaging at $62/bbl, lower vs both 2Q19 ($69/bbl), as well as 3Q18 ($76/bbl).

The US dollar strengthened for one more quarter, with average Euro/USD exchange rate at €1.11, mainly driven by central banks monetary policy.

In product markets, an important development was the drop in HSFO cracks, in contrast with other products, that were notably stronger q-o-q, leading refining benchmark margins higher vs 1H19. This trend, was sustained in 4Q19, especially for diesel, ahead of IMO regulation implementation, confirming the Group’s strategy for structural minimization of HSFO production, while increasing high value products output, through the investment in Elefsina refinery upgrade, as well as the new Aspropyrgos refinery operating model for bunkering fuels in 2020.

Urals pricing at parity to Brent, albeit with volatility during the quarter, led to weaker refining margins vs last year. FCC margins averaged at $4.9/bbl, vs $5.7/bbl in 3Q18, with Hydrocracking margins at $4.8/bbl (3Q18: $5.6/bbl).

Increasing demand for domestic fuels market

Domestic fuel demand in 3Q19 amounted to 1.6m MT (+3%), with a respective increase in auto-fuels, the highest in the last few quarters. Aviation and bunkering fuels grew significantly (+14%), mainly on account of higher marine fuel offtake (+22%).

Strong balance sheet, improved capital structure, reduction in finance costs

The new €500m Eurobond issue, at the lowest cost for the Group in more than 10 years, combined with the partial refinancing of 2021 eurobonds through a tender offer, as well as the repayment of the €325m notes in 3Q19, are expected to have a positive impact on finance costs of over €30m. Furthermore, the new issue has improved commercial terms vs previous, enhancing flexibility, while extending the Group’s maturity profile.

Net Debt at €1.5bn, significantly lower y-o-y, with gearing ratio at 39%.

Key strategic developments

Aspropyrgos refinery is planning its transition to the new operating model in November, in view of new MARPOL regulation implementation for bunkering fuels, in order to effectively respond to the new market needs. A material part of feedstock required to operate the new model has already been secured, de-risking our planning.

During October 2019 a full turnaround, involving extended maintenance at all units, was successfully completed at Elefsina refinery, safely and in line with timetable. Works are now concluded and the refinery will resume operations in the next days.

In E&P, the Greek parliament proceeded to the ratification of the Lease Agreements (effective 10 October 2019) for the offshore areas of 'West Crete' and 'Southwest Crete' (Total 40% - Operator, ExxonMobil 40%, HELLENIC PETROLEUM 20%), as well as ‘Ionio’ (REPSOL 50% - Operator, HELLENIC PETROLEUM 50%) and ‘Kyparissiakos Gulf’ (HELLENIC PETROLEUM 100%), while planned environmental and exploration studies in the other Western Greece concessions continued.

Key highlights and contribution for each of the main business units in 3Q19 were:

REFINING, SUPPLY & TRADING

Refining, Supply & Trading 3Q19 Adjusted EBITDA at €129m (-25%).

- Net production amounted to 3.8m MT (-5%), with sales at 4m MT (-1%).

- Realised ΗELPE system margin came in at $10.1/bbl, a significant recovery vs 1H19.

- During 3Q19, the IMO test run led to further diversify crude slate.

PETROCHEMICALS

- Lower PP sales (-5%), as well as inventory losses, led EBITDA to €20m (- 20%).

MARKETING

- 3Q19 Marketing Adjusted EBITDA at €51m, with 9M at €111m. Excluding the impact of IFRS 16 implementation, Comparable EBITDA was €46m (+9%), with 9M at €86m (+7%).

- In Domestic Marketing, improved performance in Retail and Aviation led 3Q19 Comparable EBITDA at €27m (+5%).

- Profitability improved in most markets the Group operates, with 3Q19 International Marketing Comparable EBITDA at €19m (+16%).

ASSOCIATE COMPANIES

- DEPA Group contribution to consolidated Net Income was €17m for 9M19.

- Higher production in both ELPEDISON plants, led EBITDA to €8m (+79%).

Notes: 1. Calculated as Reported adjusted for inventory effects and other non-operating items.

Further information:

V. Tsaitas, Investor Relations Officer

Tel.: +30-210-6302399

Email: [email protected]