5 minutes

5 minutesReported Net Income at record high of €329m, despite weaker benchmark refining margins by 25%

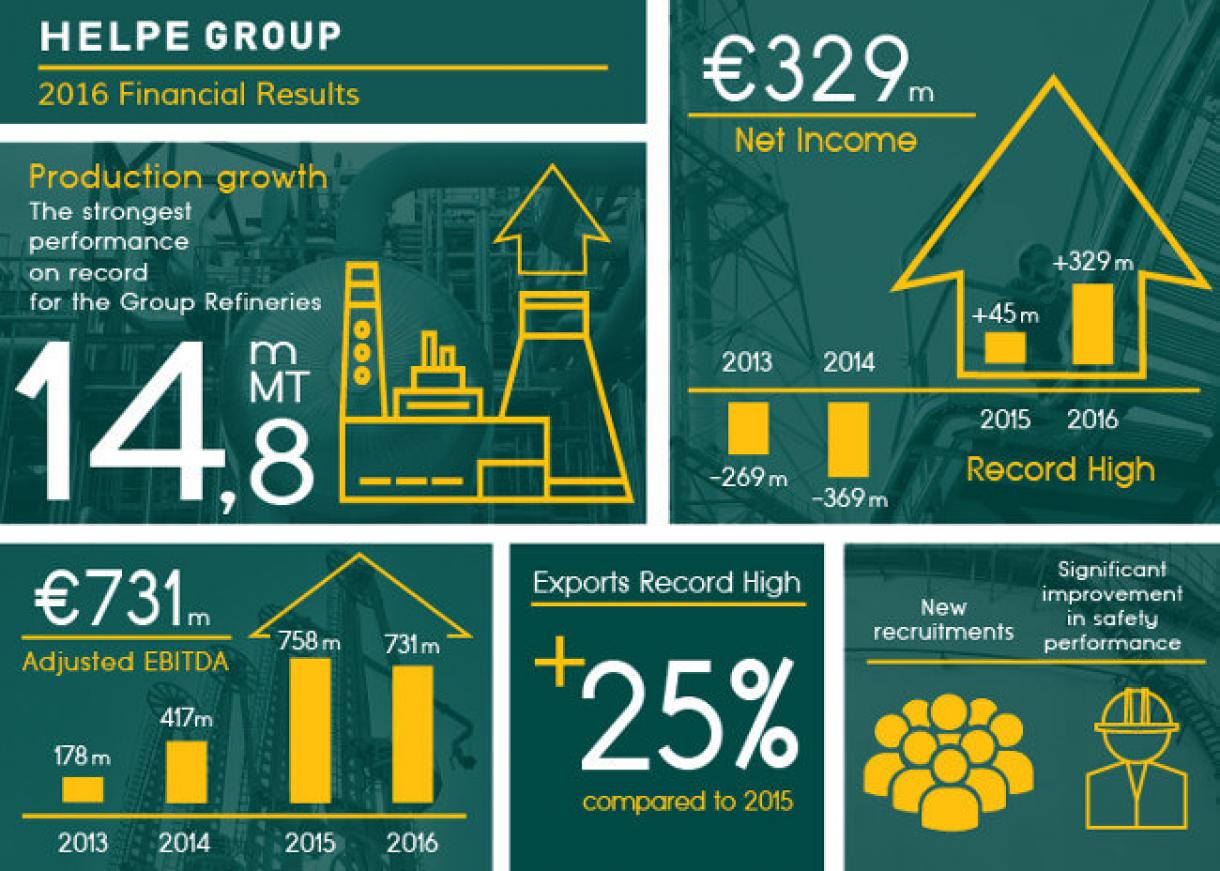

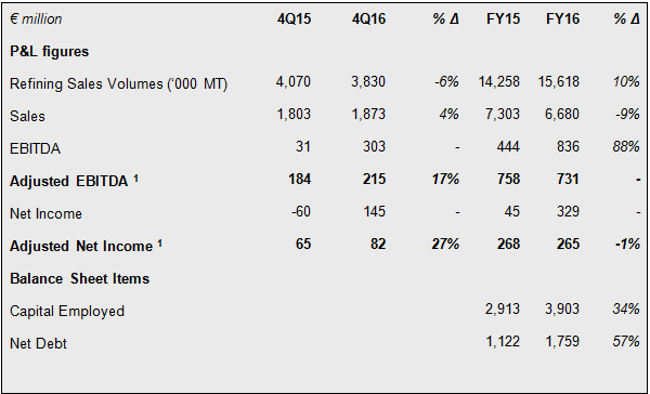

HELLENIC PETROLEUM Group announced its FY16 results, according to IFRS. In FY16, the Group achieved significantly higher profitability, for the second consecutive year, following losses in 2013 and 2014, despite a 25% drop in benchmark refining margins, reporting the strongest reported results on record; Reported EBITDA came in at €836m, while Net Income amounted to €329m, vs NI of €45m in FY15 and -€329m in FY14. Adjusted results, removing the effect of €102m of inventory gains, due to the recovery of international oil prices, were sustained for the second year at historical highs, with Adjusted EBITDA at €731m and Adjusted Net Income at €265m, vs losses of €117m in 2013 and marginal profit of €2m in 2014.

Record high production and exports

Group refineries reported a 16% production growth in FY16, at 14.8m MT, the strongest performance on record, fully capturing the high availability of units and crude optionality, recording over performance vs benchmark margins. Exports reached a historical high, at 8.6m MT, representing 56% of total sales. All Group activities reported positive results, with Petchems increasing contribution to €100m, also with higher sales. Fuels Marketing Adjusted EBITDA amounted to €100m, with most of our subsidiaries increasing their share in respective markets.

Stronger financial position, lower interest expense and stronger cash flows

During 2016 the Group, for the second consecutive year, achieved strong operating cash flows (Adjusted EBITDA – Capex) of €605m, higher vs 2015 (€593m) and significantly increased vs those of 2014 (€281m) and 2013 (€66m), further improving and de-risking Group balance sheet.

Strong operating cash flows and the improved position of the Group in financial markets, following successful negotiation and harmonisation in financial ratios and debt covenants in eurobonds and bank facilities, enabled the decrease of gross debt by €389m, which came in at €2,842m in FY16, with obvious benefits for the Group, reaffirmed by the successful issue of the new 5-year, €375m Eurobond, with a 4.875% coupon.

Furthermore, improved liquidity, combined with the agreements for direct supply from national oil companies of Russia, Iran, Iraq, Saudi Arabia and Egypt, enabled the realization of opportunities in the Med crude pricing, with significant benefits for the Group in its financial performance, operations and security of supply.

Following the improvement of balance sheet structure, total equity increased by €352m, to €2,142m. FY16 Net Debt amounted to €1,759m, with gearing ratio at 45% and capital employed at €3,903m, reflecting an improved balance sheet structure.

Increased market share in the domestic market, despite marginally lower demand

Domestic fuels demand was marginally higher by 0.26% in FY16 (ground fuels consumption lower by 0,81%, vs marine & aviation market higher by 0,91%), amounting to 10,424k MT, vs 10,451k MT in 2015.

Domestic Fuels Marketing total sales increased by 7.8%, at 3.538k MT; market share was also higher in all products ranging between 0.3% and 8.1%, with total increase of 2.4%. The development of company controlled network was also significant in 2016, with both EKO and BP penetrating the market, with high value consumer proposition in products and services.

Key strategic developments

In the context of an international tender process, HELLENIC PETROLEUM was announced as preferred bidder for the award of hydrocarbons exploration and exploitation rights in offshore “block 10” in Kyparissiakos Gulf area.

Regarding the sale process of 66% of DESFA share capital to SOCAR, it did not materialise to a transaction. The Group, in cooperation with the HRADF will assess their next steps.

Furthermore, following a tender process conducted by RAE in December 2016 for the construction of PV projects with a total capacity of 40 MW, the Group submitted successful offers for all its 3 projects, with total installed capacity of 8,6 MW. The Group will proceed with the development of these projects in the next few months.

Dividend Distribution

On the basis of the positive 2016 results and the improved financial position of the Group, the BoD of HELLENIC PETROLEUM decided to propose to the AGM the distribution of €0,20/share.

4Q16 Results – key developments

Recovery of crude oil prices

OPEC’s decision to reduce crude oil production and exports led to the recovery of international crude oil prices, with Brent averaging $51/bbl, the highest since 3Q15.

A heavier refinery maintenance schedule in 4Q16 affected products’ supply-demand balances, leading to the recovery of key product cracks q-o-q, supporting Med benchmark refining margins, with FCC averaging $5.4/bbl, vs $4,7/bbl in 4Q15 and Hydrocracking at $5.5/bbl vs $6.6/bbl last year. On a FY16 basis the two key benchmark margins came in at $5.0/bbl, $1.5/bbl lower (-25%) vs 2015.

4Q16 Results

Adjusted EBITDA amounted to €215m (+17%), with Adjusted Net Income at €82m (+27%). Higher refining contribution, on account of operational performance and strong refining margins, as well as improved performance in Petchems and Marketing were the key results drivers. Thessaloniki refinery safely and successfully completed a planned 4-week, full turnaround program, in line with schedule. The refinery was back in operation during 4Q16, with improved financial contribution.

Reported results benefited significantly from inventory gains of €82m, due to crude oil price recovery and the agreement for an insurance compensation of HELLENIC PETROLEUM relating to the post start-up operational issues of the flexicoker unit at Elefsina refinery during the 2013-14 period, with Reported Net Income at €145m.

The Group recorded another quarter of strong cash flow, with operating cash flows (Adjusted EBITDA – capex) at €171m, sustaining the balance sheet de-risking process.

Key highlights and contribution for each of the main business units in 4Q16 were:

REFINING, SUPPLY & TRADING

- Refining, Supply & Trading 4Q16 Adjusted EBITDA at €169m.

- Production amounted to 3.7 million tonnes, affected by the lower utilisation at Thessaloniki refinery, due to maintenance, with white products’ yield at 84%

- Exports amounted to 2m MT, slightly lower vs last year, accounting for 53% of total sales of 3.8m MT.

PETROCHEMICALS

- Despite weaker PP benchmark margins, Petchems profitability was sustained at high levels, with Adjusted EBITDA at €25m, while sales were 8% higher at 64k tonnes.

MARKETING

- Marketing Adjusted EBITDA in 4Q16 amounted to €20m, vs €17m LY (+17%).

- Market share gains were the key driver of Domestic Marketing profitability, with Adjusted EBITDA at €9m.

- International Marketing was affected by lower margins in Bulgaria and Serbia, with Adjusted EBITDA at €11m.

ASSOCIATED COMPANIES

- DEPA Group contribution to consolidated Net Income came in at €15m, due to significant demand increase from gas-fired electricity generators and weather conditions.

- Elpedison EBITDA at €11m in 4Q16.

Key consolidated financial indicators (prepared in accordance with IFRS) for 4Q16 are shown below:

Notes:

1. Calculated as Reported adjusted for inventory effects and other non-operating items.

Note to Editors:

Founded in 1998, Hellenic Petroleum is one of the leading energy groups in South East Europe, with activities spanning across the energy value chain and presence in 6 countries.

Further information:

V. Tsaitas, Investor Relations Officer

Tel.: +30-210-6302399

Email: [email protected]