7 minutes

7 minutes

Positive operating results, amid a negative refining environment that affects core Group business

Significant recovery of Reported profitability to the highest level in the last few years

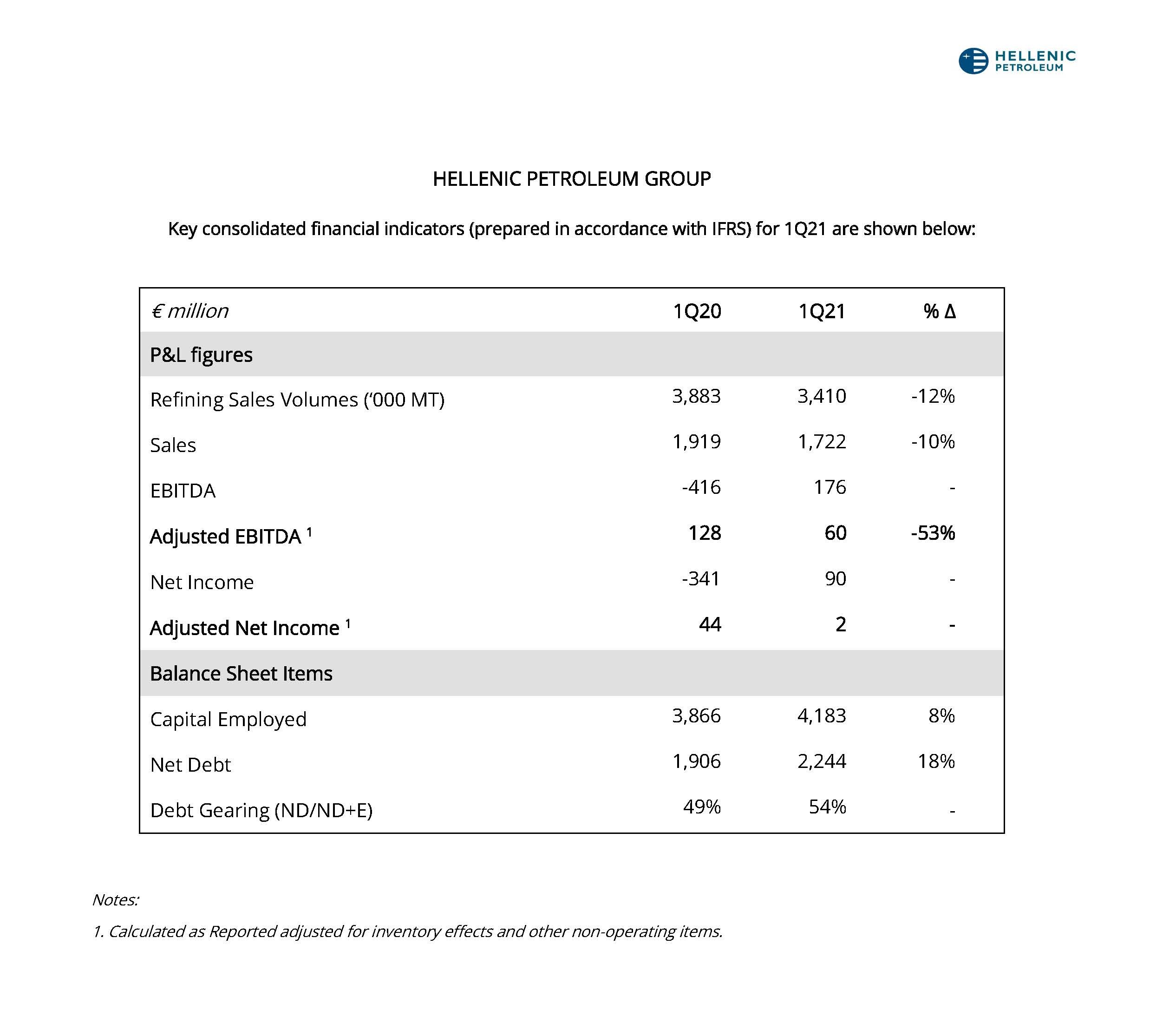

- Reported EBITDA at €176m and Reported Net Income amounting to €90m. Highest reported results since 2018.

- Satisfactory operational results, despite the adverse business environment. Adjusted EBITDA at €60m.

- Financing cost at €24m, the lowest level in recent years.

- Petrochemicals achieved its highest performance historically. Approval of a €35m investment for the PP production unit in Thessaloniki-

- Implementation of the “VISION 2025” strategy for the Energy Transition Environmental targets for net-zero by 2050.

- Targeting for 600 MW RES portfolio in operation until 2025 - will exceed 2 GW by 2030. Overall progress of the 204 MW PV large project in Kozani at 40%.

HELLENIC PETROLEUM Group announced its 1Q21 financial results, with Reported EBITDA at €176m and Reported Net Income amounting to €90m. Adjusted EBITDA came in at €60m, with corresponding Net Income at €2m.

Reported Net Income was strong, mainly driven by the international oil prices recovery and their impact on inventory valuation, offsetting a significant part of the losses recorded in 2020, when the pandemic led to a sharp price decline.

In terms of operating profitability, which excludes the impact of international crude and oil product prices, international refining performance continues to be affected by reduced transport fuels demand and especially aviation fuel, due to travel restrictions. This market segment accounts for a significant part of production and sales, prolonging a period of particularly weak refining margins.

Regarding the Greek fuels market demand, 1Q21 was the lowest on record, as restrictions on travelling were in place throughout the quarter.

In addition, following the introduction of the new EU Emissions Trading System (EU ETS), the volume of rights sourced by the market has increased materially, which, combined with their large price increase, adds significant burden on the operating costs of European refineries and their competitiveness vs non-EU countries.

In this environment, the Group maintained its good operating performance; refining utilisation, supply optimization, options on higher domestic market share and the introduction of new premium fuels in retail, as well as the highest profitability on record for Petchems, partially offset the adverse business environment.

Strategy update – Main developments

In April 2021, the Group updated its strategy, considering the accelerating energy transition, clarifying its objectives regarding Environment - Society - Governance (ESG), as well as the levers to achieve them. The new “Vision 2025” strategy is based on 5 main pillars:

- Setting clear environmental targets, including a 50% improvement in GHG emissions by 2030, with a commitment to net zero by 2050

- Adjusting the strategy to develop an additional line of business in clean energy

- Establishment of a fit-for-purpose Group structure that supports this strategy

- Upgrading corporate governance, in line with the new legal framework and international best practices

- Relaunching of corporate identity, which will highlight the new Group strategy

In the context of creating a balanced portfolio, the Group intends to drastically decarbonise its activities in the oil products value chain, through energy efficiency projects and use of cleaner forms of energy, transition to cleaner fuels and adoption of blue / green hydrogen technologies. In addition, it aims to develop a significant RES portfolio, targeting 600 MW by 2025 and 2 GW by 2030, initially in PV and onshore wind, with future expansion in offshore wind and storage applications, investing in both organically as well as through acquisitions, both in Greece and internationally. It is noted that the construction works of the 204 MW PV project in Kozani are progressing as scheduled, with approximately 40% completed.

Regarding Petchems, an investment of €35m has already been approved for the capacity increase of the PP production unit at Thessaloniki to 300k MT, targeting implementation in the next two and a half years. This investment increases the vertical integration with refining, increases Group exports and contributes to the Group’s environmental footprint improvement.

Concerning the sale process by the HRADF of the companies DEPA Infrastructure and DEPA Commercial (65% HRADF - 35% HELPE), in which the Group participates as a joint seller in DEPA Infrastructure and as a potential buyer through a joint venture with EDISON in DEPA Commercial, the submission of binding bids is scheduled for July 2021 for DEPA Infrastructure, while for DEPA Commercial the HRADF announced the suspension of the tender process until at least the end of 3Q21.

Andreas Shiamishis, Group CEO, commented on results:

«The operating environment we faced in the last 14 months has been the most difficult for years. All businesses, that operating in an economy and society that have been challenged by the pandemic and its impact, were affected and had to adapt their operations and strategy accordingly. The oil industry has been among the hardest hit, as travel restrictions continue to affect demand for our products.

As a result, despite oil prices returning to pre-crisis levels, the international refining environment records, for the fourth quarter in a row, very weak margins, while fuels demand in our key markets remains lower than normal levels. Over the coming months, we expect a substantial improvement, as the progress in vaccinations will increase domestic traffic and air travel in an important period for tourism especially for our country.

The 1Q21 results reflect this environment with low refining profitability, which due to its significant importance, outweighs improvements achieved in other Group business units. Turning on the quarter’s positive highlights, the strong IFRS profitability due to the prices’ recovery, offsets a material part of the losses recorded last year, while the continued financing costs reduction, allows the planning of a more ambitious growth plan.

In terms of strategy, there is a growing necessity to transform the Group and transition to New Energy, with investments that complement our traditional activities. The Group operates a business model set up during the ‘90s and although it has proven successful to-date, it has to adopt to changes in environmental goals, as well as expected prevailing conditions in the energy market and the economy in the coming years.

"VISION 2025" aims to position the Group as a key player in this new market, through a holistic improvement and development program, which defines our strategy in all ESG activities, investment strategy, organisational structure, corporate governance and the Group’s identity. "VISION 2025" is an ambitious roadmap, which despite the implementation challenges, is a must for the Group’s further development and will benefit all stakeholders and the Greek economy».

Crude oil prices increase and volatility of refining margins. Further increase in CO2 emission allowance prices

International crude oil prices continued to recover in the first quarter, as global demand increased and the OPEC+ crude oil production cut agreement was extended, with Brent prices averaging at $61/bbl in 1Q21, reaching $66/bbl in March, at pre-COVID-19 crisis levels.

The US dollar continued weakening vs the euro, at the lowest quarterly average of the last two years, mainly reflecting monetary policy; euro came in at 1.20 in 1Q21.

CO2 emission allowance prices were significantly higher, exceeding €40/MT at the end of 1Q21, at a multiple compared to the last 3 years. This increase, combined with the reduction of allowances for European manufacturing, is a competitive disadvantage for the European refiners, with operational and strategic implications.

Gasoline cracks increased slightly due to demand recovery, while middle distillates remained at multi-year lows as aviation demand is still weak. Brent-Urals margin strengthened against the lows of the previous three quarters; as a result, FCC margins averaged at $2/bbl, with Hydrocracking margins at $-0.1/bbl.

Weak domestic market demand

Domestic fuel demand in 1Q21 was 14% lower, at 1.5m MT, with auto-fuels consumption recording an even higher decline of 16%, due to the mobility restrictions in the first quarter of the year. Heating gasoil demand also decreased by 10% due to mild weather. Bunkering fuels demand amounted to 575k MT (-4%), with significant drop in aviation (-69%).

Strong balance sheet, financing cost reduction

Following the successful refinancing of €900m credit facilities, the Group significantly improved its financing mix, increasing the percentage of committed credit lines and expanding their maturity profile. In addition, the financing cost in 1Q21 amounted to €24m, the lowest level in recent years, falling below €100m on an annual basis. Regarding the refinancing of bonds maturing in October ’21, amounting to €200m, the Group is reviewing its options, considering the “2025 Vision” strategy program.

Net Debt came in at €2.2bn, mainly due to the increase of international prices and higher working capital.

Key highlights and contribution for each of the main business units in 1Q21 were:

REFINING, SUPPLY & TRADING

- Refining, Supply & Trading 1Q21 Adjusted EBITDA at €6m.

- Production at 3.4m MT (-13%), with respective sales which came in at 3.4m MT (-12%).

- HELPE’s system flexibility allowed the materialisation of opportunities in the IMO fuel trading and production optimization at Aspropyrgos refinery.

PETROCHEMICALS

- Petrochemicals achieved its highest performance historically, capturing strong PP margins, with Adjusted EBITDA amounting to €36m (+ 84%) in 1Q21.

- HELPE’s BoD approved the investment of €35m to increase the capacity of the polypropylene plant in Thessaloniki, by 25%, to 300k MT.

MARKETING

- In domestic marketing, cost control efforts and improved operational performance with the introduction of the new 98-octane gasoline in the EKO petrol station network, mitigated the impact of weak demand for auto and aviation fuels, with the 1Q21 Adjusted EBITDA at €11m.

- In international marketing, the results were mainly affected by the significant sales volumes decline due to travel restrictions which led 1Q21 Adjusted EBITDA to €10m.

ASSOCIATE COMPANIES

- DEPA Group contribution to 1Q21 consolidated Net Income came in at €11m.

- ELPEDISON 1Q21 EBITDA was 37% higher, at €23m, due to due to improved performance of the upgraded Thessaloniki plant and exploitation of gas trading opportunities.

View here the above table on pdf